Water management spend for hydraulic fracturing is forecasted to average US$17 billion from 2019 through 2028, according to new market forecasts from Bluefield Research. Emboldened by growing demand for scaling water supplies and disposal needs, a host of midstream water companies backed by private equity and sovereign wealth funds are positioned to seize the opportunity going forward.

According to Bluefield’s new report, Midstream Water Management: U.S. Hydraulic Fracturing Strategies, Solutions, & Outlook, water management for the fracking sector has maintained a steady clip since 2017. Spend on water supply, transport, treatment, storage, and disposal has increased 12% per year from US$11.74 billion to a projected US$15.49 billion by the close of 2019.

“Water management does not just start and stop at the frack, which underpins the recent growth in the midstream water management and a wave of investment from 30+ private equity and financial firms,” says Reese Tisdale, President of Bluefield Research. “The significant share of transport costs to the industry has ushered in more than 57 water management firms—pure-play water players, energy services companies, and technology promoters—along the industry value chain.”

The lion’s share of activity has been in the Permian Basin, where 47% active horizontal drill rigs are located. Eight of the ten most active counties in the U.S. are in the Permian Basin, which spans West Texas and Eastern New Mexico. Over the last two years, Bluefield has identified more than 30 water transfer projects in the Permian Basin, alone, targeted at addressing water transfers for fracking.

With oil prices ranging from US$50.88 to US$64.93 over the last year, and what some consider a softening in the market, demand for midstream water management still remains robust. The combination of more efficient drilling practices and increased water demand per well—sometimes reaching 15 million gallons—creates significant water volume demand.

Confidence in water for fracking intensified in 2015 when global energy markets spiraled toward sub-$40 per barrel prices. Water management, as a result, began making up a larger share of industry wallet, let alone increased public scrutiny. Bluefield has identified 69 acquisitions of companies active in managing water and produced water (wastewater). While some of the earlier deal flow stemmed from the consolidation of struggling and bankrupt companies, more recent activity, such as Blackstone’s and Singapore-based GIC US$3.3 billion investment, signals greater interest.

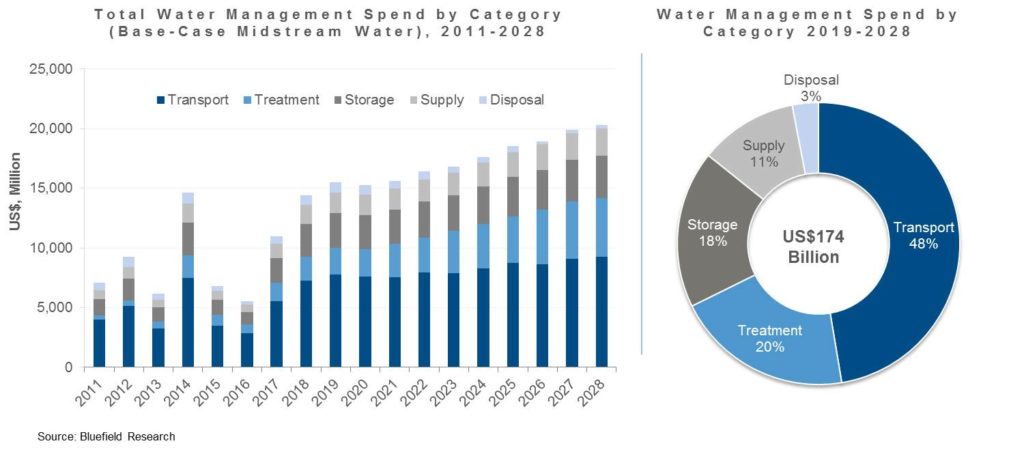

Bluefield’s analysis indicates two fundamental shifts since the last market collapse: The overall resiliency to price swings of upstream oil & gas in the U.S. has increased for water service providers, thereby encouraging increased investment in related infrastructure; Secondly, water management strategies have zeroed-in on water transfers, which make up approximately 49% of total water management spend.

“That said, our team recognizes the mercurial nature of energy markets that is substantiated historically in the water for fracking sector’s relatively short existence. For this reason, Bluefield has laid out critical levers of change in the development of four forecast scenarios—Market Collapse, Water Scarcity, Midstream Water, and Drill, Baby, Drill!. At their extremes, these varying outlooks demonstrate a US$86 million swing that accounts for potential geopolitical, regulatory, and economic shifts that influence market dynamics.”