According to the latest IDA Desalination Yearbook, in the first half of 2017, the water sector produced 99,758 billion m3/day of desalinated water throughout the planet.

The current year, 2018, appears to be on track to become one of the record years in terms of contract volume, due to the size of the new mega desalination plants launched in the Near East, such as Taweelah (900,000 m3/d), Rabigh (650,000 m3/d) or Shuqaiq 3 (450,000 m3/d), with just these three plants accounting for a cumulative capacity of 2,000,000 m3/d of desalinated water. The trend appears to be following along this trail, as shown in the attached projections.

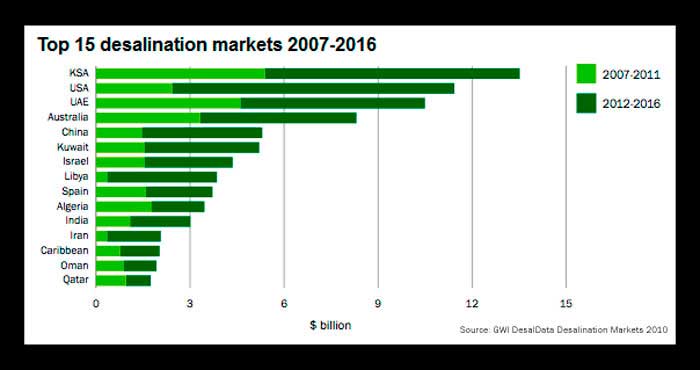

Desalination as a mature technology for the generation of drinking or industrial water has spread significantly. Currently, desalinated water is produced around the world by more than 20,000 facilities of different sizes. This large number includes from small production focused on residential or private industrial areas (between 50 and 600 m3/day) to large plants that supply municipal utilities that use desalinated water as a primary source or for mixing with other drinkable resources for distribution to the population or industry. Today, the largest plants are located in the United Arab Emirates, Saudi Arabia, Algeria and Israel.

Saudi Arabia has some of the largest desalination facilities in the world, combining different technologies (MED, MSF and RO), including the Shoaiba project, which produces 880,000 m3/day, and the Al Jubail complex, which produces more than 800,000 m3/day. The Sorek project in Israel is currently the largest seawater reverse osmosis desalination plant in operation, with a capacity of 624,000 m3/day, followed by the Magtaa plant in Algeria, with a production of 500,000 m3/day. But these figures will change soon after the projects mentioned earlier go into operation.

The water sector produced 99.758 billion m3/day of desalinated water throughout the planet.

With this evolution, desalination technology has matured, while production and operating costs have dropped, water quality parameters have improved and energy costs (which represent the largest part of the cost structure) have decreased.

In order to properly analyze the evolution of production costs over the years, we are going to focus on the rates of plants operating under the BOOT scheme. Today, 50% of the desalination plants are contracted under this model and the demand is increasing thanks to the balance in the distribution of the risks, which makes very competitive rates possible.

The first desalination plants developed under the BOOT model were small reverse osmosis facilities built in the early 1980s on the Mediterranean and in the Caribbean, and thermal technology projects associated with power plants in the Near East. During the 1990s, this model became more popular because private water companies began to develop opportunities around the world.

The decrease in costs has been one of the principal factors in the acceptance, growth and success of desalination. Since the 1960s, the cost of Multistage Flash Distillation (MSF) to desalinate water has dropped by around 90%, from approximate unit costs of 10 US$/m3 in the 1960s to less than 1 US$/m3 in 2010. Even in 2017, in some places, the cost of MSF has decreased up to an additional 20% with respect to 2010 due to technological development and lower energy prices.

Currently, the average price range of desalinated water is between 0.5 US$ and 1.5 US$/m3. The lower end of this range includes the regions with lower electricity costs (for example, the Middle East) and at the high end, we found the regions with higher electricity costs (for example, Australia, where electricity is sometimes required to be generated using renewable energies).

It is hard to analyze production costs if we isolate them from the scenario in which they are produced, so in this article, we will do it from the perspective of geography and time.

Mediterranean

The desalination market in the Mediterranean was a pioneer in the introduction of reverse osmosis technology. It started in the 1990s with small-scale plants to supply drinking water to hotels and resorts in the Balearic and Canary Islands. Supply prices were higher than 1.5-2 US$/m3, but there were also no other reference prices. The first price references per m3 of desalinated water were launched by the government of Cyprus through the Water Development Department of Cyprus, through 20-year contracts. Projects such as Limassol, Larnaca and Dhekelia were the first BOOT projects in the sector, and since then, they have been expanding in terms of capacity and new locations. The contracts for these first projects were awarded for more than one dollar in 1995.

The local experience, the presence of qualified personnel in the country, technological know-how and energy optimization are the main factors that made it possible to reduce the rates for desalinated water in the zone. Examples of this decrease include the Larnaca projects, with rates in 2001 of 0.74 US$/m3 and Limassol in 2012 with 0.87 US$/m3, with the lowest price in the country achieved in October 2018, when the Paphos desalination plant with a capacity of 20,000 m3/d was awarded to the local contractor Caramondani for 0.51 US$/m3.

Spain began its own desalination plan in the 1990s, and for two decades developed a program of more than 1 million m3/day under the EPC model, charged to the national and regional government budgets, with the support of European funds. This was the first large-scale desalination program using membrane technology and all of the Spanish companies in the sector participated, later exporting their experience to other countries to make them leaders in the market today.

There is no reference rate for those years, but we do have an indication of the investment per m3 installed, which varies widely depending on the design, size, specifications and conditions of the civil and marine works. The cost of the plants for each 100,000 m3/day installed also evolved from initial projects of more than $115-117 million, to $70-80 million for the latest plants constructed, which are larger and use more mature technology. After years of development and construction of plants, the operation of medium and long-term contracts ranged between 0.20 and 0.36 US$/m3.

In parallel, the most important projects at the time were launched in Israel, in terms of both size as well as their technological advances: Askhelon (396,000 m3/d) with a rate of 0.52 US$/m3; Hadera (525,000 m3/d) at 0.58 US$/m3; and Sorek (624,000 m3/d) at 0.58 US$/m3. The reality is that these were disruptive rates, but we now know that they were conditioned by inflated parameters and that when updated to today’s values, they represent rates of around 0.95 - 0.89 – 0.7 US$/m3 respectively.

In addition, Algeria launched its own desalination plan to resolve the water supply problem that the coastal zones in the north were experiencing. This first development consisted of the construction of 40 small reverse osmosis plants with capacities between 400 and 2,000 m3/day. The plants were delivered and put into operation, but unfortunately the plan did not work due to the lack of training and knowledge of the operating staff. Most of these plants were shut down and forgotten due to lack of maintenance.

In 2005, Algeria launched an ambitious new program that became a point of reference for the sector. Very well-structured projects, with very competitive debt available from local banks and rates in dollars. Likewise, to reassure shareholders, it was agreed that the main national energy companies, Sonatrach and Sonelgaz (through a company created for this purpose: AEC) acted as guarantors and held participation in the mixed companies of the consortium that was awarded each project. Under this arrangement, 12 desalination projects were launched in less than 10 years. The first plants were Hamma (200,000 m3/d) with a rate of 0.78 US$7m3 and Skikda (100,000 m3/d) with a rate of 0.739 US$/m3. Later came Beni Saf (200,000 m3/d) at 0.78 US$/m3 and Honaine (200,000 m3/d) at 0.69 $/m3; to finish with Magtaa (500,000 m3/d) and Ténès (200,000 m3/d), which were contracted with practically the same debt and energy costs below 0.57 US$/m3.

On their part, Tunisia, Egypt and Morocco also developed their own small and medium-sized projects during the first decade of the century. In Morocco, after many years contracting under EPC in regions such as Tan Tan, Bouchra and El Aaiún, the first desalination plant under the BOOT model was launched by the ONEP (National Office of Drinking Water), in Agadir, with a capacity of 100,000 m3/d and contracted at a rate of 0.87 US$/m3.

Asia and the United States

In Asia, Singapore, Australia, India and China are perhaps the countries that stand out most in terms of the development of desalination programs, although the latter two are not very transparent in communicating the production costs, and the available data is very dispersed. The two ground-breaking projects in this area were Chennai and Qingdao, both with a capacity of 100,000 m3/d contracted under a BOOT scheme and with rates of 1.03 US$/m3 and 0.71 US$/m3. After this, rates have been variable, but the project structures do not provide the minimum bases of international bankability in terms of guarantees and consumption, so the data cannot be taken into consideration for the purposes of comparison.

In Singapore, for many years there has been a single company for the development of desalination projects, with an evolution of prices from 0.89 US$/m3 to 0.36 US$/m3 for the “Tuasspring” plant in 2013, but with significant problems due to the aggressive rate policy that this company was applying in the sector. The new and most recent expansion launched by the National Water Agency of Singapore (PUB) Tuas III was contracted by a new player in the company at a rate of 0.54 US$/m3.

Australia is another leader in desalination, although it works with development models that are significantly different. This is an area with a higher level of specifications and redundancies and with more demanding construction systems than those found in other regions, which means that the production prices per m3 are not comparable. However, we do have the example of the Melbourne plant, with a capacity of 450,000 m3/d and which was contracted for 0.89 US$/m3 in 2015.

Lastly, we have the United States, which, although it is not a world leader in large seawater desalination plants, is one of the largest producers of water by reverse osmosis from brackish water. Most of its consumption is for industrial uses and/or small municipalities, but it does have some large developments, such as the ones in Tampa, Florida, and Carlsbad and Huntington Beach in California. The first, in Tampa Bay, encountered numerous problems, including the bankruptcy of the construction company, which had to be replaced during the construction phase.

The projects in California are characterized by their long environmental approval periods and exaggerated development costs of more than 40 MM USD. In the case of Carlsbad, its engineering and construction model increased the investment to move the project forward to more than 700 MM USD. In addition, the plant received a subsidy from the state of California and with all of this, there are exercises that indicate that the equivalent rates of these desalination plants are higher than 3-4$ per m3, which is far outside of the market range in other parts of the world.

Middle East

The Middle East is the leader in desalinated water production in the world, with current production of 6.5 million m3/day and a trend that is on track to double this value in the coming years. Saudi Arabia alone produces between 4 and 5 million m3 a day, with a plan to reach 9 million m3/day in the next 10 years. In terms of production capacity, it is followed by Kuwait, United Arab Emirates and Oman. The main reasons for this lead include its extreme climate conditions and the absence of water resources.

In terms of technology, the most widely used up until a few years ago were Multiple Effect Distillation (MED) and Multistage Flash Distillation (MSF), whose primary product is energy and the condensed water appears in the secondary production process. When the priority is water production, the plant must remain operational, regardless of whether the energy produced is needed or not, so it is very difficult to quantify the production cost per cubic meter. But starting in 2011, there was a change in the trend and membrane desalination technology took the lead, achieving lower investment and operating costs, as shown in the attached table.

In the last year, the market in the region has launched the world’s largest desalination projects based on reverse osmosis. The progress and experience with the technology (in terms of its engineering as well as the local construction capabilities), the effect of scale, maturity in project structuring, the appetite of private investors and the liquidity of the debt market are breaking the rate barriers, bringing them to the lowest levels possible.

- 2018 September – Rabigh (Saudi Arabia) 660,000 m3/d: 0.55 US$/m3

- 2018 October - Taweelah (United Arab Emirates) 909,000 m3/d: 0.49 US$/m3

- 2018 November - Shuqaiq (Saudi Arabia) 450,000 m3/d: 0.52 US$/m3

This means that as of today, we can say that desalination is a mature technology with competitive production costs and attractive investment returns for investors, in addition to being a viable solution that is on the rise to combat the problems of water scarcity in all areas of the planet. Investing in desalination means investing in health, economy and development.

Sources:

- The Cost of Desalination, Advising WorleyParsons Group.

- Desalination and water treatment: A Review on Energy Consumption of Desalination Processes. Younes Ghalavand, Mohammad Sadegh Hatamipour, Amir Rahimi.

- El consumo de energía en la desalación de agua de mar por ósmosis inversa: situación actual y perspectivas. Antonio Esteban and Manuel García Sánchez Colomer.

- Global Water Intelligence. Volume 12, Issue 12, December 2011.

- GWI & IDA Desal Data.